Before I try to explain it, here are some fun facts

- Only 13% of the workforce is currently covered by pension schemes

- Total government (centre+states) pension cost has increased from Rs 6,400 crore in 1991 to Rs 46,569 crore in 2001 and it is estimated that this figure will reach around 80000 crores by 2081-82

- A number of states are already defaulting on pension payments. Employee Pension Scheme was reportedly underfunded to the extent of Rs 22,000 crore as on March 31, 2004.

Essentially, the PFRDA bill aims to address all of the above. This Bill provides a regulatory framework for a new pension system (NPS) which will be available to any individual. All the employees who joined the central government on or after 1 January 2004 already come under this new pension system.

Details

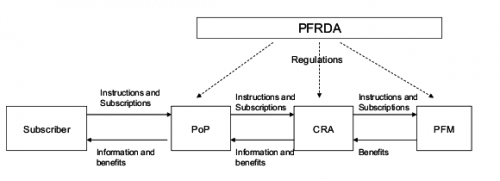

The bill establishes the Pension Fund Development and Regulatory Authority (on the lines of RBI,SEBI, TRAI), defines its powers and duties, and defines the outline of New Pension System(NPS). In essence PFRDA shall regulate this new pension system.

- The system comprises one (or more) central record-keeping agency (CRA), a set of pension fund managers (PFMs) and point-of-presence agencies (PoPs).

- The CRA shall maintain records, accounts and effect all instructions regarding subscription, switching of options and withdrawals by the subscribers. The subscriber may access the CRA directly for information.

- The PFMs shall provide a set of schemes with varying risk-return profiles (i.e. balance between risk taken and returns expected), and manage the assets of subscribers.

- The PoPs shall receive instructions and contributions from subscribers, transmit these to the CRA, and pay out benefits to the subscribers. PoPs will be the “windows” for subscribers to the system.

- Every subscriber shall have an individual pension account (IPA). He has the option of selecting the PFMs and schemes. He can switch his funds across PFMs and schemes.

- The IPA will be portable in case of change of employment. (As in the case of a bank account, the IPA is independent of employment details). The subscriber cannot exit from the system except on certain conditions.

Current System Vs Proposed System

The current pension system, a defined benefit (DB) system, promises a fixed amount to be paid per month as pension. This amount is linked to the pay drawn, number of years of service etc., and has no direct linkage to the contribution of the employee or employer towards a pension fund. Thus, the entire investment risk is borne by the pension fund manager and the government. However, the employee is exposed to the risk that the total benefits liable are higher than the funds available, which can lead to delays and defaults.

In the new pension system, a defined contribution (DC) system, each employee (and his employer in the case of government servants appointed since 2004) contributes a proportion of his monthly income to an individual account. This account is invested in one or more schemes offered by pension fund(s). The balance in the account belongs to the employee, which will be accessible at the time of exit. The employee bears the entire investment risk. However, there is no risk of default by the fund as the liability of the fund to its subscriber equals the assets owned by it.

| Current System | Proposed System |

|

1. Guaranteed retirement income 2. Returns fixed depending on pay drawn, years of service. |

1. Returns are subject to market performance. 2. Employees may benefit from better returns |

| 3. Employees do not bear any investment risk. | 3. Employees bear investment risk and may make misinformed choices. |

| 4. Employees do not have any choice in investing. | 4. Employees have more choice in investing.They have option to switch fund managers and schemes |

| 5. Fund manager could default if funds are not invested appropriately | 5. No risk of default by fund managers |

| 6. Less portable in switching employers | 6. Plans are portable across job changes |

| 7. Not beneficial to employees who leave before minimum eligible service | 7. Years of service do not matter, but it is difficult to build a fund for those who enter the system late in life |

Highlights of the bill

- NPS will cover Central government employees who joined after 1 January 2004. State governments may mandate NPS. The Bill makes the NPS available to the unorganized and private sector but does not make it mandatory.

- It is estimated that NPS will lead to savings of Rs 1,000 crore in the year 2039-40 which will increase to Rs 37,000 crore by 2059-60 which will further increase to Rs 72,000 crore by 2081-82.

- An inherent risk is that any unfavourable event affecting market prices at the time of retirement could lower both pension wealth and the annuity rate. Subscribers may have to stay on in the system beyond their retirement date in order to ride over such a shock.

Updates

- According to the PFRDA website, it seems that 19 states have already issued notifications that they are moving to NPS.

- I came across a press release by PFRDA which says that NPS has been opened to all citizens from May 1, 2009.

- I also checked out the PFRDA website and looks like besides the usual suspects LIC, SBI, UTI other private players like ICICI, Kotak and Reliance have also come on board as Pension Fund Managers.

Questions

- Can NPS be used to ensure that every working citizen, public sector or private/organized or unorganized, is covered under a pension scheme?

- Does it make government jobs a little less attractive? ;)

I am attaching the bill draft, a comprehensive yet simple legislative brief prepared by PRS and the press release by PFRDA which I have mentioned. All the information is available at PRS site here

-Shekhar

ಪ್ರತಿಕ್ರಿಯೆಗಳು

Non-pension retirees

There is a category of retirees from public sector who were not eligible for any pension when they retired after a life time of service with meagre PF/Gratuity which got washed out in no time due to inflation and reduction in bank interest rates.

They have been pleading with the Govt. to no avail.

K.V.Pathy